Repeat after me - the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector. The housing market is red hot right now, and yet builders are loathe to invest in a major way, fearing a downturn that will impact their profit margins, even though they stand to make big bucks. But we somehow expect a building surge that will shift the market dynamics to make all housing worth less?

The only way to incentive construction is to incentive construction. NYC HPD is an agency, for example, that has a history of providing low interest rate loans for approved projects to rehab old buildings. With borrowing costs hovering at 8%-10% for new construction projects, and with lenders tightening standards, this is the perfect time for state governments and the federal government to provide 3% construction loans, accessed in tranches after milestones are met, to facilitate not only housing on the cheaper end of the spectrum, but lower-margin housing projects that established developers and big lenders typically shy away from.

Simply deregulating does not work, and it's foolish to think it would. Lower cost housing, made profitable by public lenders as a last resort, is a no-brainer that gets lost in the discussion. As is rent control, by the way. But that won't lead to the same cast of characters getting boffo bucks through deregulation, so neither option is taken seriously by Serious People.

Sorry to be harsh, but what planet was this written from? The housing market in the US is largely frozen - many people bought at peak prices over the pandemic years at rock bottom interest rates, so now they basically can't move - they simply can't afford the same amount of house at today's rates, and many would have to lower their prices in an attempt to sell in this higher rate market. The fact that employment is still relatively high means most people aren't forced to sell, and thus prices remain unaffordably high in many cities.

Edit: And rent control? Virtually every economist of all ideological stripes agrees that rent control is ultimately self defeating in the long term. And just look what happens with people that live in rent-controlled cities. Families hang on to those apartments like they're diamonds, and all it does is create a world of "haves vs. have nots", where it's like a big lottery to get a rent controlled apartment, but meanwhile you've disincentivized builders from building any new stock.

It depends on the area. There are still areas in the United States where demand is still incredibly high, meaning homes sell above asking or 50+% more than 10 years ago

An example includes areas outside of the NYC metro area. Sure they aren't get peak pandemic prices but they are still getting crazy amounts of money for a home that was worth 50% less 10 years ago.

It was just a bubble. Austin was the ultimate "meme stock" during the pandemic years. Austin has a lot of good things going for it, but between things like Musk, Joe Rogan, "crypto bros", tons of Silicon Valley decampers, it just got way over-hyped.

One of the things Austin always had going for it was that it was a good value compared to bigger cities, but now that it's just about as expensive as those bigger cities, people are realizing the brutally hot summers, lack of easy access to mountains or oceans, relatively bland architecture and abysmal public transportation just make it overpriced.

Maybe be a little less pedantic and engage in good faith - of course by "red hot" I meant that sellers can name their price, with sales still often going above asking in many regions across the US. Prices shot up like a rocket ship since the beginning of the pandemic, have been remarkably durable, and still continue to climb.

OK, I'll be less pedantic. I think it's just flat out wrong.

It was a red hot market about a year and a half ago. Prices were shooting up, and there was a frenzy of buying, with lots of people feeling FOMO for not buying a house. The situation now is completely different.

Housing prices rarely, rarely go down without widespread unemployment because people are so loath to sell at a loss. So the situation is a bit odd right now it that so many people can't move because interest rates are so high, but unemployment is still low so people aren't forced to sell. The reason prices have stayed relatively flat is because for the small amount of inventory that has come on the market there's still little reason to sell at a loss. That's still the opposite of any definition of a hot market.

> Edit: And rent control? Virtually every economist of all ideological stripes agrees that rent control is ultimately self defeating in the long term. And just look what happens with people that live in rent-controlled cities. Families hang on to those apartments like they're diamonds, and all it does is create a world of "haves vs. have nots", where it's like a big lottery to get a rent controlled apartment, but meanwhile you've disincentivized builders from building any new stock.

That “unanimous” agreement is starting to change and outside the US there was never unanimity on the subject.

As per usual it is an issue that has already been tackled by other nations but that we in the US insist is a “uniquely American” issue.

In countries that have a constitutions that don’t read like a product of an eleventh hour scramble to finish a homework assignment, that is to say, most western countries, they’ve chosen to enshrine certain human rights in their constitution.

Like the right to accessible housing.

This serves as a mandate for the government to enable this.

In most countries, although details can differ, this translates to strong tenant protections and market-wide rent control.

Having those two points at the foundation will literally negate any argument raised against rent control in the US.

If it’s market-wide then there are no haves and have nots, everyone is a have.

Another argument that’s often thrown around is that landlords would stop investing in the upkeep of property, but in a society with strong tenant protections and market-wide rent control that prospect simply doesn’t exist.

Why?

Because the rent control is often based on a point system that sets the price and the tenant protections require a certain standard of living.

If the property isn’t kept up the landlord will receive less rent, or hell, in egregious cases no rent at all.

You’ll see that with that stick behind the door, all of a sudden the landlord is perfectly capable to keep their properties up to par.

Another thing that’s thrown around often is that there wouldn’t be any incentive to build more housing.

Never mind the fact that in those countries this notion that the sky will come falling down has yet to come to fruition, it’s often the very same American real estate investment companies that are warning for the end of times here in the US if tenant protections and rent control will be passed, that are building and buying up rental properties over there.

In fact, the same issue here, conglomeration of big corporate landlords, is becoming an issue there. Often these corporations are American and lately also Chinese.

So it seems that landlords there still have a huge appetite, despite the strong tenant protections, strong tenant unions and strong rent control, all of which are even far beyond what is proposed here in the US.

Because the real fact of the matter is, that as long as profit can be made, however small, people will still try to make that profit and not, like you and others are suggesting, just call it quits.

This is because it simply depends on what is “normal” and in the US we need a new “normal” like the one on those other countries.

And let’s be clear, that “normal” is still nothing to sneeze at, this despite the cost of construction being significantly higher in many of those countries as well as the corporate taxes that are involved.

What we need in the US is more willingness to look at our peers and see how they’ve handled certain issues.

But the main problem is the lack of political will, across the spectrum, to actually deal with these issues, because of corporate money being pumped around into political pockets.

Which is a topic for another time I suppose.

"Nothing great was ever built without a speculative bubble." -- Fred Wilson

The way this normally works out is that the price goes up; the high price attracts many independent firms into the market; these firms all go gangbusters trying to supply the market to cash in on the money in the sector; they solve the supply problem; the market ends up being oversupplied as all the new firms keep building; prices crash; lots of these firms declare bankruptcy; and then their resources are redeployed in the next speculative bubble.

If you're talking about "the private housing sector" or "the builders" as a monolithic entity, you've already lost. There should be individual builders who all respond to price incentives and build what the market demands, not a cartel of builders who have the ability to dictate local policy & prices.

I agree with you - that's why I propose public corporations as lenders of last resort to create incentives outside of the traditional market forces that would help create this housing stock that industry insiders would rather not.

> yet builders are loathe to invest in a major way

This is not true in areas that make it easy to build housing. The reality is that builders are loath to get caught up in NIMBY bullshit that stops them from building after they dump a million on bureaucratic nonsense, not that they are trying to protect housing prices.

They are built on land that is relatively scarce (in suburban areas, and the UK scarce full stop), zoned by local government, subject to the influence of regulations and unions etc.

House builders in the UK quite clearly hold back on (or try to corrupt their way out of) large developments that require them to build social housing, they seem to have slowed down building in response to threatened law changes around leaseholds (which are onerous and abusive), and they appear to hold back on smaller projects as leverage with local governments in discussions about the regulations that are stopping them taking on larger projects.

They are absolutely willing to build fewer houses than they could, and they tend to be rewarded for this with higher prices, because the barriers to entry in building houses at scale are really significant.

The problem is land. The private sector isnt going to make new land. Nobody makes land. Not in the private sector. It'll build apartments on freed up land but it won't make new land.

If private investors dont lose money on inefficiently used land then they will hoard it as jealously as a goldbug hoards gold or a crypto bro hoards bitcoin.

Right now one theoretically could build a mansion in London with 100 rooms and pay $1500/year in property taxes. This isnt theoretical. I live about a kilometer away from a Russian oligarch who did exactly that and that is indeed how little he pays in tax on it.

We can either jack up property taxes or jack up land taxes but either way until land hoarding is made a shortcut to bankruptcy then the housing crisis will only ever get worse.

We used to build cities in America. Our grandparents' generation got brand new roads, brand new houses, brand new schools, etc. There is a concept of being at capacity, and there are areas that have reached that capacity, where the roads can comfortably carry X number of cars, where density is enough to support a local economy and industry, and the quality of life is good. Rather than trying to cram 5 pounds of crap into a 10 pound bag, building new cities in proximity to economic megalopolises (first as a crutch to support the population of the new city) with easy transportation between the two is something that California has a great track record of, for example, that you don't see in the Northeast. Irvine is a great semi-recent example of that. This is development done correctly, not cramming as many people into a mature area as possible, and then whining that NIBMYism makes living there expensive when the infrastructure of a city or region is at capacity.

And what happens when you can't build anymore, like on the island of Manhattan? You regulate rents to protect housing for the economically-diverse population of people who live there. This is all not that complicated, but all we hear about is this deregulation model that doesn't make any sense when you game it out two steps ahead.

>Rather than trying to cram 5 pounds of crap into a 10 pound bag

This is what you call living in high rises in cities like Manhattan or San Francisco?

>There is a concept of being at capacity

Capacity which tax policy has been designed to artificially throttle. It doesn't really matter if the market wants to build high rises 15 minutes from the offices in SF and people want to live in high rises 15 minutes from work if a stick in the mud lives there in a $6 million bungalow he inherited from his mom who bought it in 1974.

Obviously if he were taxed a bit higher for occupying valuable land he would sell up and leave and those apartments could be built. But, why not indulge the NIMBY desire to be "at capacity"? Those NIMBYs probably worked hard for that $6 million by buying in the 90s or by being pushed out of the vagina of somebody who did.

If you actually had experience living or working in Manhattan, you’d see that it has the infrastructure to enable density - namely, the country’s most intricate and heavily-used subway and transit system, by a mile. (17x the ridership compared to the next largest, Chicago.) But yeah, let’s build density without discussing how we rebuild cities with transit and how we pay for this multi-decade endeavor that will conservatively cost tens of billions per city. It’s almost like the half-baked “solution” of deregulation doesn’t actually make sense once you analyze it for five minutes, oh and it’s the preferred, and only, policy pushed hard by developers. Funny how that works.

You characterize the private sector as a monolithic decision-making entity, like the government. That’s a fundamental misunderstanding and mischaracterization. There is a collection of fiercely competing interests that balances. Right now, everyone who is able to build a new house is doing so, at significant profit interest. There’s an entire subsector of the economy that is “developers and home builders.” Do you presume these people somehow sit on their hands at the command of some other group?

> the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector.

> yet builders are loathe to invest in a major way, fearing a downturn that will impact their profit margins, even though they stand to make big bucks.

The second quote doesn’t flow from the first. The second quote is correct - builders aren’t building not because they don’t want to tank housing prices, but because of concerns about the economy. In a capitalist system with thousands of players, it there are expectations of profits there will be construction even if it drives down the profits of the industry as a whole (that’s the free market, eliminating excess profits). The issue has nothing to do with mass collusion to keep prices high and everything to do with concerns about the economy and the current interest rate environment.

The second quote isn't entirely related to the first. "Sufficient housing stock to tank prices" is an enormous amount of housing, the likes of which are not contemplated by traditional builders, who are out to build high profit margin housing at prices the market will bear. That's the system that needs disruption. It's not de jure collusion, it's a mature industry with mature players who have been on the search for blockbuster profits in recent memory. The average home size has skyrocketed over the last forty years, builders and their financiers are no longer content to make a living building homes, they want to hit home runs every time. It's time to incentivize smaller players in the market and to steer them towards building cheaper housing with smaller profit margins.

> fearing a downturn that will impact their profit margins

The obvious answer is for the Fed to give clear guidance on when rates can go back to dropping. There's no mystery why builders are pulling back; people can't get mortgages.

We don't need a new complicated system, there are easy fiscal knobs to turn.

They cannot do this because doing so would eliminate the ambiguous feedback loop on “expectations” that is intended to exist and ultimately under their credibility in the longer run.

Not sure what data you're looking at, but that's completely off. Trailing 12 month food inflation is over 4%. Transportation inflation is over 10%. Services excluding energy are up 5.9%.

The boom gets started with an expansion of credit.

The fed sets rates low, are you starting to get it?

That new money is confused for real loanable funds,

but it’s just inflation that’s driving the ones

who invest in new projects,

like housing construction.

The boom plants the seeds for its future destruction.

The savings aren’t real,

consumption’s up too!

And the grasping for resources reveals there’s too few.

https://youtu.be/d0nERTFo-Sk?si=mcHcwlGi-TPaf5q-

The claim being that to back a loan with new “printed” money is necessarily inflationary.

Loans backed with saved/invested funds are non-inflationary, because the saver gives up their ability to consume with those funds, in proportion with the consumption the borrower takes on.

Housing barely appreciates above inflation. About 4% on average, yearly. It would be better if we didn't interfere in the market, or there are going to be some nasty consequences.

And yet housing has outpaced wages exponentially for decades - that's the appropriate comparison, not the stock market or inflation with a broader index.

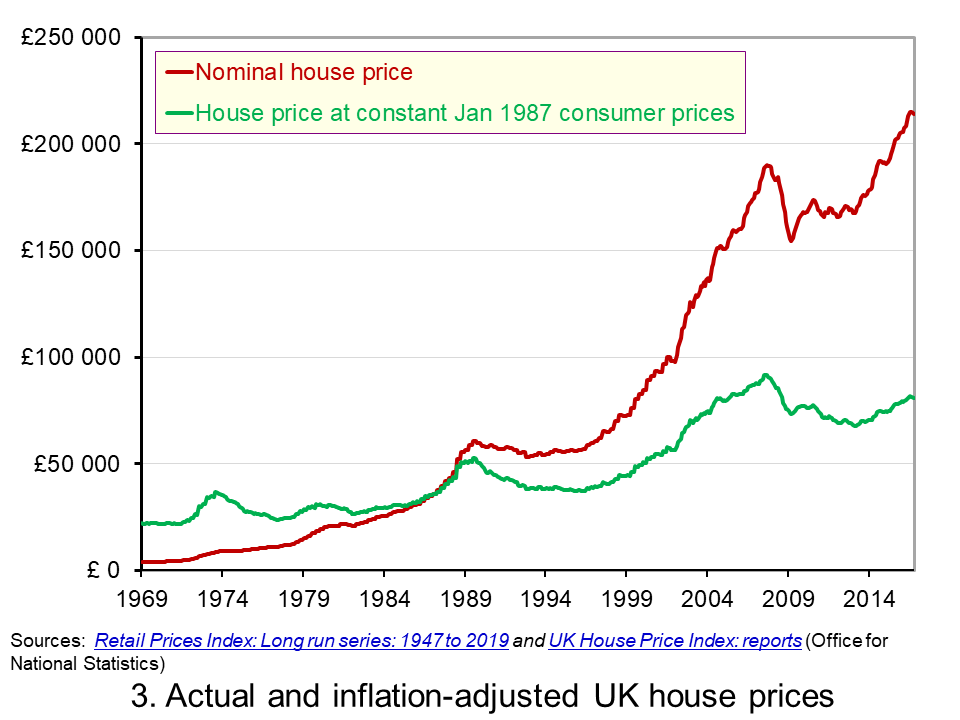

Kiwi moved to the UK and housing market is just insane here, not even just London. Not only have house prices outpaces inflation (lack of new being built, housing being used as "investments" etc) but also stagnant wages.

The only reason I'll ever be able to afford a smallish house here is being on a tech salary; take average London wage here...and without generational wealth transfer they _cannot_ buy a house. Even with generational wealth transfer, our London salary friend will have to buy a house _outside_ london and commute (or wfh).

It's not a "hot market" it's just the haves have a vested interest in keeping the prices high for the have-nots. Just look at how landlords reacted to tenants getting some basic rights (that we've had in NZ for ages) "the sky is falling".

And all of this is for terraced houses at best, sharing a wall with neighbours, not detached at all, maybe you get a backyard maybe not. All made out of brick and built in the 40s-60s for the most part - and falling apart because of this. Never have I seen so much scaffolding since I moved to the UK.

There are still a few great things about living in the UK, but the housing market (amongst other things, wage gap, classism, corruption, population political apathy) is an absolute disgrace.

You're saying they're wrong that housing barely appreciates above inflation, around 4%, citing as an example a relative's sale of a house held for 50 years for 7.5x the real price.

Care to take a guess what 4% compounded for 50 years is? It's +611% or a total of 7.1x the original price. Your relative experienced 4.11% annual real gains, pretty close to 4%.

Over the last 70 years, a 300% gain in real terms is an annual increase of just 2%. That is barely outpacing inflation in my book.

> Over the last 70 years, a 300% gain in real terms is an annual increase of 2%. That is barely outpacing inflation in my book.

Your barely ain't my barely, that is for sure.

Compared to any other form of retail investment an average UK consumer could make instead (assuming they still also need to pay for accommodation), 2% over inflation consistently over that period is very significant. 4% over inflation is surely massive. (Particularly since the last 15 years of consumer savings yields have barely matched inflation, as I understand it; no matter, since the average consumer has not been able to save meaningfully since 2008 anyway).

As a store of consumer wealth in the UK, there is nothing even remotely close to housing.

There is an HN worldview distortion where buying a house is something really almost everyone here can hope for, and having the kind of resources and risk capacity to access opportunities with greater than 4% interest is not unusual.

In that same 70 year time period, the S&P 500 total return was 1234x against a USD inflation figure of 11.5x, for a real return of 107.3x or a real return CAGR of 6.9% versus the 2% CAGR that housing appreciated.

Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will also crush housing, just as the SP500 does in the US.

> There is an HN worldview distortion where buying a house is something really almost everyone here can hope for

In the US, ~2/3 of households own their homes, almost identical to the UK figures.

> Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will crush housing.

Yeah of course, after they have paid for their endlessly rising rent (because they aren't buying a house in this comparison, are they). And all their bills, and their food, and their energy.

Sorry: average UK people aren't investors, and nor are average Americans. This is the bias I am talking about. You're just not thinking the same way I am thinking. You are in a box where people have money to make investments.

> In the US, ~2/3 of households own their homes, almost identical to the UK figures.

Wrong way to look at it though. In the UK, the vast majority of people under 40 do not have a mortgage.

A majority of those people will never own a property. Even if their parents own a property, they are not particularly likely to inherit enough of a share of that money to secure a deposit on a house, because they are likely to have siblings and their parents are likely to have had to release equity to pay for their elderly care or pay bills.

Some but by no means most parents die with enough savings that an only child can inherit the house after all the taxes are paid; the average house price is very close to the IHT threshold.

The _average_ deposit in the UK is now 15%. That, combined with the fact that the average person in the UK is bearing down on 50 when they do inherit and will tend to need a higher deposit than a first time buyer...

4% above inflation is a dream.

I guess in the USA you still have little boxes being built on virgin hillsides. That is over in the UK; it's been over for 25 years. The limited supply of housing in the UK in the last 50 years will absolutely blow you away.

> Indeed, if someone spends everything they earn, they can neither invest nor save up a downpayment to buy a property.

This is, at a first approximation, everyone in the UK right now who does not already have a mortgage. A majority of people in the UK are spending more than they earn at the moment (for at least some months this year). And almost no mortgage holders are saving in anything other than employer pensions.

Just shy of 10% of UK mortgage holders will even have missed a mortgage payment at least once this year.

> Repeat after me - the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector.

This. In the UK in particular there are so few housebuilders working at scale that they effectively have an oligopoly. And they turn off the tap as quickly as OPEC do.

Are these groups impairing their future profit interest, discounted at the cost of capital, by building more homes? You assert the answer is ‘yes.’ Why?

It doesn't take much imagination to understand that the handful of companies who control house-building and therefore house prices might have a variety of reasons to slow down the building of houses that have nothing do to with direct profit.

Because they exert power over more than just the market price by doing so.

But since you're imagining words into my mouth you ought to have the imaginative capacity to figure that out for yourself.

{kind=link}

The only way to incentive construction is to incentive construction. NYC HPD is an agency, for example, that has a history of providing low interest rate loans for approved projects to rehab old buildings. With borrowing costs hovering at 8%-10% for new construction projects, and with lenders tightening standards, this is the perfect time for state governments and the federal government to provide 3% construction loans, accessed in tranches after milestones are met, to facilitate not only housing on the cheaper end of the spectrum, but lower-margin housing projects that established developers and big lenders typically shy away from.

Simply deregulating does not work, and it's foolish to think it would. Lower cost housing, made profitable by public lenders as a last resort, is a no-brainer that gets lost in the discussion. As is rent control, by the way. But that won't lead to the same cast of characters getting boffo bucks through deregulation, so neither option is taken seriously by Serious People.