Repeat after me - the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector. The housing market is red hot right now, and yet builders are loathe to invest in a major way, fearing a downturn that will impact their profit margins, even though they stand to make big bucks. But we somehow expect a building surge that will shift the market dynamics to make all housing worth less?

The only way to incentive construction is to incentive construction. NYC HPD is an agency, for example, that has a history of providing low interest rate loans for approved projects to rehab old buildings. With borrowing costs hovering at 8%-10% for new construction projects, and with lenders tightening standards, this is the perfect time for state governments and the federal government to provide 3% construction loans, accessed in tranches after milestones are met, to facilitate not only housing on the cheaper end of the spectrum, but lower-margin housing projects that established developers and big lenders typically shy away from.

Simply deregulating does not work, and it's foolish to think it would. Lower cost housing, made profitable by public lenders as a last resort, is a no-brainer that gets lost in the discussion. As is rent control, by the way. But that won't lead to the same cast of characters getting boffo bucks through deregulation, so neither option is taken seriously by Serious People.

Sorry to be harsh, but what planet was this written from? The housing market in the US is largely frozen - many people bought at peak prices over the pandemic years at rock bottom interest rates, so now they basically can't move - they simply can't afford the same amount of house at today's rates, and many would have to lower their prices in an attempt to sell in this higher rate market. The fact that employment is still relatively high means most people aren't forced to sell, and thus prices remain unaffordably high in many cities.

Edit: And rent control? Virtually every economist of all ideological stripes agrees that rent control is ultimately self defeating in the long term. And just look what happens with people that live in rent-controlled cities. Families hang on to those apartments like they're diamonds, and all it does is create a world of "haves vs. have nots", where it's like a big lottery to get a rent controlled apartment, but meanwhile you've disincentivized builders from building any new stock.

It depends on the area. There are still areas in the United States where demand is still incredibly high, meaning homes sell above asking or 50+% more than 10 years ago

An example includes areas outside of the NYC metro area. Sure they aren't get peak pandemic prices but they are still getting crazy amounts of money for a home that was worth 50% less 10 years ago.

It was just a bubble. Austin was the ultimate "meme stock" during the pandemic years. Austin has a lot of good things going for it, but between things like Musk, Joe Rogan, "crypto bros", tons of Silicon Valley decampers, it just got way over-hyped.

One of the things Austin always had going for it was that it was a good value compared to bigger cities, but now that it's just about as expensive as those bigger cities, people are realizing the brutally hot summers, lack of easy access to mountains or oceans, relatively bland architecture and abysmal public transportation just make it overpriced.

Maybe be a little less pedantic and engage in good faith - of course by "red hot" I meant that sellers can name their price, with sales still often going above asking in many regions across the US. Prices shot up like a rocket ship since the beginning of the pandemic, have been remarkably durable, and still continue to climb.

OK, I'll be less pedantic. I think it's just flat out wrong.

It was a red hot market about a year and a half ago. Prices were shooting up, and there was a frenzy of buying, with lots of people feeling FOMO for not buying a house. The situation now is completely different.

Housing prices rarely, rarely go down without widespread unemployment because people are so loath to sell at a loss. So the situation is a bit odd right now it that so many people can't move because interest rates are so high, but unemployment is still low so people aren't forced to sell. The reason prices have stayed relatively flat is because for the small amount of inventory that has come on the market there's still little reason to sell at a loss. That's still the opposite of any definition of a hot market.

> Edit: And rent control? Virtually every economist of all ideological stripes agrees that rent control is ultimately self defeating in the long term. And just look what happens with people that live in rent-controlled cities. Families hang on to those apartments like they're diamonds, and all it does is create a world of "haves vs. have nots", where it's like a big lottery to get a rent controlled apartment, but meanwhile you've disincentivized builders from building any new stock.

That “unanimous” agreement is starting to change and outside the US there was never unanimity on the subject.

As per usual it is an issue that has already been tackled by other nations but that we in the US insist is a “uniquely American” issue.

In countries that have a constitutions that don’t read like a product of an eleventh hour scramble to finish a homework assignment, that is to say, most western countries, they’ve chosen to enshrine certain human rights in their constitution.

Like the right to accessible housing.

This serves as a mandate for the government to enable this.

In most countries, although details can differ, this translates to strong tenant protections and market-wide rent control.

Having those two points at the foundation will literally negate any argument raised against rent control in the US.

If it’s market-wide then there are no haves and have nots, everyone is a have.

Another argument that’s often thrown around is that landlords would stop investing in the upkeep of property, but in a society with strong tenant protections and market-wide rent control that prospect simply doesn’t exist.

Why?

Because the rent control is often based on a point system that sets the price and the tenant protections require a certain standard of living.

If the property isn’t kept up the landlord will receive less rent, or hell, in egregious cases no rent at all.

You’ll see that with that stick behind the door, all of a sudden the landlord is perfectly capable to keep their properties up to par.

Another thing that’s thrown around often is that there wouldn’t be any incentive to build more housing.

Never mind the fact that in those countries this notion that the sky will come falling down has yet to come to fruition, it’s often the very same American real estate investment companies that are warning for the end of times here in the US if tenant protections and rent control will be passed, that are building and buying up rental properties over there.

In fact, the same issue here, conglomeration of big corporate landlords, is becoming an issue there. Often these corporations are American and lately also Chinese.

So it seems that landlords there still have a huge appetite, despite the strong tenant protections, strong tenant unions and strong rent control, all of which are even far beyond what is proposed here in the US.

Because the real fact of the matter is, that as long as profit can be made, however small, people will still try to make that profit and not, like you and others are suggesting, just call it quits.

This is because it simply depends on what is “normal” and in the US we need a new “normal” like the one on those other countries.

And let’s be clear, that “normal” is still nothing to sneeze at, this despite the cost of construction being significantly higher in many of those countries as well as the corporate taxes that are involved.

What we need in the US is more willingness to look at our peers and see how they’ve handled certain issues.

But the main problem is the lack of political will, across the spectrum, to actually deal with these issues, because of corporate money being pumped around into political pockets.

Which is a topic for another time I suppose.

"Nothing great was ever built without a speculative bubble." -- Fred Wilson

The way this normally works out is that the price goes up; the high price attracts many independent firms into the market; these firms all go gangbusters trying to supply the market to cash in on the money in the sector; they solve the supply problem; the market ends up being oversupplied as all the new firms keep building; prices crash; lots of these firms declare bankruptcy; and then their resources are redeployed in the next speculative bubble.

If you're talking about "the private housing sector" or "the builders" as a monolithic entity, you've already lost. There should be individual builders who all respond to price incentives and build what the market demands, not a cartel of builders who have the ability to dictate local policy & prices.

I agree with you - that's why I propose public corporations as lenders of last resort to create incentives outside of the traditional market forces that would help create this housing stock that industry insiders would rather not.

> yet builders are loathe to invest in a major way

This is not true in areas that make it easy to build housing. The reality is that builders are loath to get caught up in NIMBY bullshit that stops them from building after they dump a million on bureaucratic nonsense, not that they are trying to protect housing prices.

They are built on land that is relatively scarce (in suburban areas, and the UK scarce full stop), zoned by local government, subject to the influence of regulations and unions etc.

House builders in the UK quite clearly hold back on (or try to corrupt their way out of) large developments that require them to build social housing, they seem to have slowed down building in response to threatened law changes around leaseholds (which are onerous and abusive), and they appear to hold back on smaller projects as leverage with local governments in discussions about the regulations that are stopping them taking on larger projects.

They are absolutely willing to build fewer houses than they could, and they tend to be rewarded for this with higher prices, because the barriers to entry in building houses at scale are really significant.

The problem is land. The private sector isnt going to make new land. Nobody makes land. Not in the private sector. It'll build apartments on freed up land but it won't make new land.

If private investors dont lose money on inefficiently used land then they will hoard it as jealously as a goldbug hoards gold or a crypto bro hoards bitcoin.

Right now one theoretically could build a mansion in London with 100 rooms and pay $1500/year in property taxes. This isnt theoretical. I live about a kilometer away from a Russian oligarch who did exactly that and that is indeed how little he pays in tax on it.

We can either jack up property taxes or jack up land taxes but either way until land hoarding is made a shortcut to bankruptcy then the housing crisis will only ever get worse.

We used to build cities in America. Our grandparents' generation got brand new roads, brand new houses, brand new schools, etc. There is a concept of being at capacity, and there are areas that have reached that capacity, where the roads can comfortably carry X number of cars, where density is enough to support a local economy and industry, and the quality of life is good. Rather than trying to cram 5 pounds of crap into a 10 pound bag, building new cities in proximity to economic megalopolises (first as a crutch to support the population of the new city) with easy transportation between the two is something that California has a great track record of, for example, that you don't see in the Northeast. Irvine is a great semi-recent example of that. This is development done correctly, not cramming as many people into a mature area as possible, and then whining that NIBMYism makes living there expensive when the infrastructure of a city or region is at capacity.

And what happens when you can't build anymore, like on the island of Manhattan? You regulate rents to protect housing for the economically-diverse population of people who live there. This is all not that complicated, but all we hear about is this deregulation model that doesn't make any sense when you game it out two steps ahead.

>Rather than trying to cram 5 pounds of crap into a 10 pound bag

This is what you call living in high rises in cities like Manhattan or San Francisco?

>There is a concept of being at capacity

Capacity which tax policy has been designed to artificially throttle. It doesn't really matter if the market wants to build high rises 15 minutes from the offices in SF and people want to live in high rises 15 minutes from work if a stick in the mud lives there in a $6 million bungalow he inherited from his mom who bought it in 1974.

Obviously if he were taxed a bit higher for occupying valuable land he would sell up and leave and those apartments could be built. But, why not indulge the NIMBY desire to be "at capacity"? Those NIMBYs probably worked hard for that $6 million by buying in the 90s or by being pushed out of the vagina of somebody who did.

If you actually had experience living or working in Manhattan, you’d see that it has the infrastructure to enable density - namely, the country’s most intricate and heavily-used subway and transit system, by a mile. (17x the ridership compared to the next largest, Chicago.) But yeah, let’s build density without discussing how we rebuild cities with transit and how we pay for this multi-decade endeavor that will conservatively cost tens of billions per city. It’s almost like the half-baked “solution” of deregulation doesn’t actually make sense once you analyze it for five minutes, oh and it’s the preferred, and only, policy pushed hard by developers. Funny how that works.

You characterize the private sector as a monolithic decision-making entity, like the government. That’s a fundamental misunderstanding and mischaracterization. There is a collection of fiercely competing interests that balances. Right now, everyone who is able to build a new house is doing so, at significant profit interest. There’s an entire subsector of the economy that is “developers and home builders.” Do you presume these people somehow sit on their hands at the command of some other group?

> the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector.

> yet builders are loathe to invest in a major way, fearing a downturn that will impact their profit margins, even though they stand to make big bucks.

The second quote doesn’t flow from the first. The second quote is correct - builders aren’t building not because they don’t want to tank housing prices, but because of concerns about the economy. In a capitalist system with thousands of players, it there are expectations of profits there will be construction even if it drives down the profits of the industry as a whole (that’s the free market, eliminating excess profits). The issue has nothing to do with mass collusion to keep prices high and everything to do with concerns about the economy and the current interest rate environment.

The second quote isn't entirely related to the first. "Sufficient housing stock to tank prices" is an enormous amount of housing, the likes of which are not contemplated by traditional builders, who are out to build high profit margin housing at prices the market will bear. That's the system that needs disruption. It's not de jure collusion, it's a mature industry with mature players who have been on the search for blockbuster profits in recent memory. The average home size has skyrocketed over the last forty years, builders and their financiers are no longer content to make a living building homes, they want to hit home runs every time. It's time to incentivize smaller players in the market and to steer them towards building cheaper housing with smaller profit margins.

> fearing a downturn that will impact their profit margins

The obvious answer is for the Fed to give clear guidance on when rates can go back to dropping. There's no mystery why builders are pulling back; people can't get mortgages.

We don't need a new complicated system, there are easy fiscal knobs to turn.

They cannot do this because doing so would eliminate the ambiguous feedback loop on “expectations” that is intended to exist and ultimately under their credibility in the longer run.

Not sure what data you're looking at, but that's completely off. Trailing 12 month food inflation is over 4%. Transportation inflation is over 10%. Services excluding energy are up 5.9%.

The boom gets started with an expansion of credit.

The fed sets rates low, are you starting to get it?

That new money is confused for real loanable funds,

but it’s just inflation that’s driving the ones

who invest in new projects,

like housing construction.

The boom plants the seeds for its future destruction.

The savings aren’t real,

consumption’s up too!

And the grasping for resources reveals there’s too few.

https://youtu.be/d0nERTFo-Sk?si=mcHcwlGi-TPaf5q-

The claim being that to back a loan with new “printed” money is necessarily inflationary.

Loans backed with saved/invested funds are non-inflationary, because the saver gives up their ability to consume with those funds, in proportion with the consumption the borrower takes on.

Housing barely appreciates above inflation. About 4% on average, yearly. It would be better if we didn't interfere in the market, or there are going to be some nasty consequences.

And yet housing has outpaced wages exponentially for decades - that's the appropriate comparison, not the stock market or inflation with a broader index.

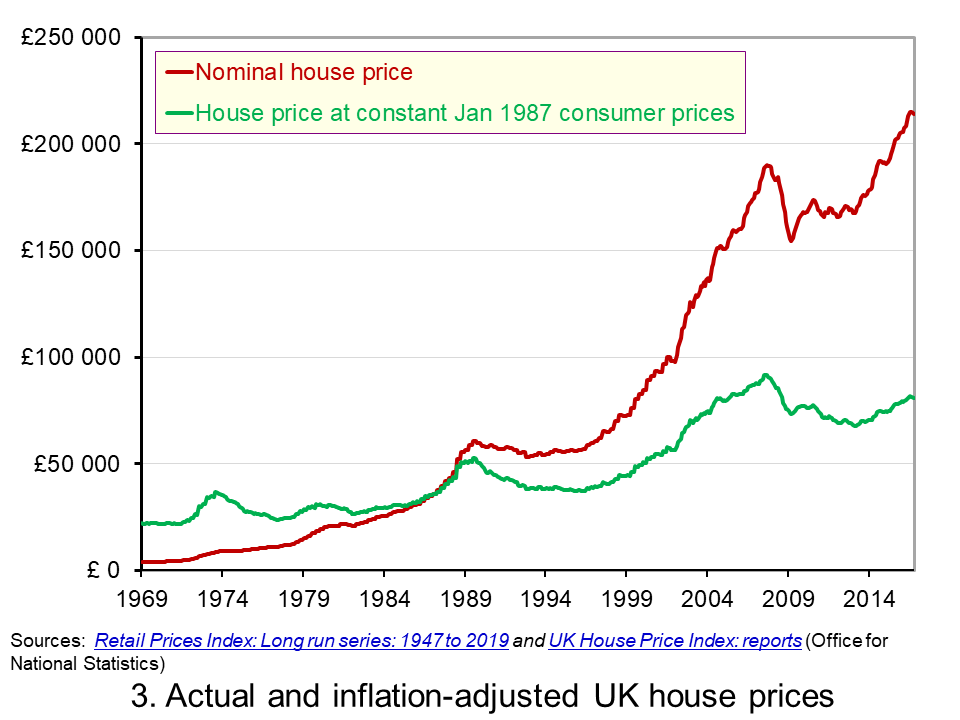

Kiwi moved to the UK and housing market is just insane here, not even just London. Not only have house prices outpaces inflation (lack of new being built, housing being used as "investments" etc) but also stagnant wages.

The only reason I'll ever be able to afford a smallish house here is being on a tech salary; take average London wage here...and without generational wealth transfer they _cannot_ buy a house. Even with generational wealth transfer, our London salary friend will have to buy a house _outside_ london and commute (or wfh).

It's not a "hot market" it's just the haves have a vested interest in keeping the prices high for the have-nots. Just look at how landlords reacted to tenants getting some basic rights (that we've had in NZ for ages) "the sky is falling".

And all of this is for terraced houses at best, sharing a wall with neighbours, not detached at all, maybe you get a backyard maybe not. All made out of brick and built in the 40s-60s for the most part - and falling apart because of this. Never have I seen so much scaffolding since I moved to the UK.

There are still a few great things about living in the UK, but the housing market (amongst other things, wage gap, classism, corruption, population political apathy) is an absolute disgrace.

You're saying they're wrong that housing barely appreciates above inflation, around 4%, citing as an example a relative's sale of a house held for 50 years for 7.5x the real price.

Care to take a guess what 4% compounded for 50 years is? It's +611% or a total of 7.1x the original price. Your relative experienced 4.11% annual real gains, pretty close to 4%.

Over the last 70 years, a 300% gain in real terms is an annual increase of just 2%. That is barely outpacing inflation in my book.

> Over the last 70 years, a 300% gain in real terms is an annual increase of 2%. That is barely outpacing inflation in my book.

Your barely ain't my barely, that is for sure.

Compared to any other form of retail investment an average UK consumer could make instead (assuming they still also need to pay for accommodation), 2% over inflation consistently over that period is very significant. 4% over inflation is surely massive. (Particularly since the last 15 years of consumer savings yields have barely matched inflation, as I understand it; no matter, since the average consumer has not been able to save meaningfully since 2008 anyway).

As a store of consumer wealth in the UK, there is nothing even remotely close to housing.

There is an HN worldview distortion where buying a house is something really almost everyone here can hope for, and having the kind of resources and risk capacity to access opportunities with greater than 4% interest is not unusual.

In that same 70 year time period, the S&P 500 total return was 1234x against a USD inflation figure of 11.5x, for a real return of 107.3x or a real return CAGR of 6.9% versus the 2% CAGR that housing appreciated.

Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will also crush housing, just as the SP500 does in the US.

> There is an HN worldview distortion where buying a house is something really almost everyone here can hope for

In the US, ~2/3 of households own their homes, almost identical to the UK figures.

> Surely, a UK investor can invest in the S&P 500 today. Go do the same math for the FSTE 100; I suspect it will crush housing.

Yeah of course, after they have paid for their endlessly rising rent (because they aren't buying a house in this comparison, are they). And all their bills, and their food, and their energy.

Sorry: average UK people aren't investors, and nor are average Americans. This is the bias I am talking about. You're just not thinking the same way I am thinking. You are in a box where people have money to make investments.

> In the US, ~2/3 of households own their homes, almost identical to the UK figures.

Wrong way to look at it though. In the UK, the vast majority of people under 40 do not have a mortgage.

A majority of those people will never own a property. Even if their parents own a property, they are not particularly likely to inherit enough of a share of that money to secure a deposit on a house, because they are likely to have siblings and their parents are likely to have had to release equity to pay for their elderly care or pay bills.

Some but by no means most parents die with enough savings that an only child can inherit the house after all the taxes are paid; the average house price is very close to the IHT threshold.

The _average_ deposit in the UK is now 15%. That, combined with the fact that the average person in the UK is bearing down on 50 when they do inherit and will tend to need a higher deposit than a first time buyer...

4% above inflation is a dream.

I guess in the USA you still have little boxes being built on virgin hillsides. That is over in the UK; it's been over for 25 years. The limited supply of housing in the UK in the last 50 years will absolutely blow you away.

> Indeed, if someone spends everything they earn, they can neither invest nor save up a downpayment to buy a property.

This is, at a first approximation, everyone in the UK right now who does not already have a mortgage. A majority of people in the UK are spending more than they earn at the moment (for at least some months this year). And almost no mortgage holders are saving in anything other than employer pensions.

Just shy of 10% of UK mortgage holders will even have missed a mortgage payment at least once this year.

> Repeat after me - the private housing sector is not going to build sufficient housing stock to tank prices in... the private housing sector.

This. In the UK in particular there are so few housebuilders working at scale that they effectively have an oligopoly. And they turn off the tap as quickly as OPEC do.

Are these groups impairing their future profit interest, discounted at the cost of capital, by building more homes? You assert the answer is ‘yes.’ Why?

It doesn't take much imagination to understand that the handful of companies who control house-building and therefore house prices might have a variety of reasons to slow down the building of houses that have nothing do to with direct profit.

Because they exert power over more than just the market price by doing so.

But since you're imagining words into my mouth you ought to have the imaginative capacity to figure that out for yourself.

For anyone who just reads the headline, and doesn't get to the first paragraph: Yes, if the new housing you are building is an increase in total stock. (I doubt that it's very often not the case, but still an important caveat).

If you tear down a high rise to build a mansion, no that won't decrease prices just because you built something new. Again, I realize that this probably almost never happens, but it's important to point out that the thing that matters is the change in stock, not the newness.

I don't know if it's just me but for some strange reason I can never get past the captcha on archive.ph. It just refreshes the page and I can never access the archived version

Build all the luxury housing you want. My first cheap slumlord apartment started its life as a luxury building in the 1930s.

The problem is when someone knocks down a 3-flat row house and builds a single family home in the same plot of land. Unless we have negative population growth that should never happen (and usually the places where knocking down a house and building an entirely new one makes sense are growing and desirable).

More often than not this happens because the denser housing predates zoning restrictions. When that building reaches end of life and needs to be replaced, there's little economic choice but to build the single-family home.

In many (most?) places, you can replace an existing non-conforming/grandfathered use with a new building that's no more non-conforming than the current situation.

As far as I know, where I live, you can do this if the old non-conforming use was destroyed due to a disaster. Otherwise maybe you can ask nicely and get lucky.

I dunno. When they built a bunch of cottages that rented for $1300 a month down the road from me that made me reconsider the $750 /month that I rent a unit in my other house for.

That is, I think seeing high prices for new developments being advertised on signs all over the place has a powerful psychological effect of creating a "level set" and even if it doesn't really drive prices up, I think many people believe that it drives prices up through that mechanism. It might be the triumph of pataphysics (e.g. in my mind the "physics" of the imagination) over economics but in the hyperreal world, pataphysics wins.

And, while supply is still constraining, landlords can get away with that. But the closer supply gets to being "not constraining", the less ability they have to do that. But, as long as supply is constrained, that will happen no matter what. While a new expensive development can be a trigger, in the absense of that trigger, someone else will realize that they can just raise prices and the market will bear it, so something else will serve as the trigger. The only way to break out of it is build enough that the power to do this goes away. Unfortunately, that is, in many of the most supply constrained areas, a huge, daunting task that will probably take years of dramatically increased development.

I own a farm which has two houses on it. I didn't decide to get in the landlord business, I got into it because the person I bought my farm from built a house for his retired mom. He rented out two units out in it after she passed away and so do I.

I am not always thinking "how do I maximize the value of my rental property?" instead it is something that comes to my mind because some kind of event happened. For instance I had a tenant who for some perverse reason didn't want to pay his well-below-market rate (because I hadn't been raising it all this time) and as a result of that we all found out what a great deal he was getting -- only after we got a lawyer involved did this guy realize he's about to paying a lot more to a slumlord for a much worse place.

There are a lot of people renting a granny flat or half a duplex or otherwise are not economically maximizing who are very much affected when they see prices advertised that are close to twice what they are renting at. Those people are side-by-side on the market with people who are using software to absolutely maximize what they can charge.

But as you point out, for market forces to overcome pataphysical forces (maybe what Thiel calls mimetic?) it will take a big change in conditions.

In Ithaca, NY we are building huge amounts of both market rate and affordable housing, enough that the skylines of downtown and Collegetown are completely transformed but it hasn't make a dent in the homeless colony despite a strong effort to get people into shelters and into housing and they are still saying it is the most expensive small city in the US, but for all I know we could be building much more.

There was an article in NYT (I think) recently that talked about how over the past 50 years or so that there was a reduction in something like 50k apartments in NYC because of people buying neighboring apartments and combining them.

It wont increase stock if you tear down a block of public housing that housed 180 and build an apartment block with 160 investments for Arab sheikh portfolios and 40 middle income apartments with a poor door.

Until land or property is taxed high enough to discourage hoarding the shortage will only get worse, even if supply trickles up. Housing is supply constrained.

As rents and prices go up the incentive to use politics to inhibit further construction also goes up. This is how a hundred residents can turn up to a city meeting in SF and demand that a launderette be declared historic.

Housing as investment only makes sense in a supply constrained environment, and, as far as I've seen, the evidence that significant amounts of housing is being held empty for investments (foreign or otherwise) is pretty scarce. It's a popular narrative that doesn't seem to be supported by the data. Build enough, and housing wont' be an investment anymore. As it shouldn't be.

That being said, I'm definitely also in favor of an LVT

In my UMC area that was formerly MC there are a lot of tear-down rebuilds that trade one single family home for another. They barely increase stock ( though the houses probably have more bedrooms).

Living in a crusty old part of NY, I would argue replacing old appt buildings with new ones, even perhaps with a slight reduction in number of units, could still reduce housing costs....

Is there really a significant number of apartments that are vacant due to habitability reasons? I believe there are a lot of vacant units out there even in hot markets, for various reasons, but mostly perfectly livable.

The best solution to this problem is taxing land value instead of taxing property. Land value taxes have a lot of advantages. They incentivize construction, disincentivize vacant lots, and they also remove the profit that can be earned by being an idle landlord, which is unearned income.

With property tax, improvements on your property are taxed. This makes construction less profitable / housing more expensive. With a land value tax, they aren't.

LVT also encourages nimbyism from people who don't want to move. If the value of their land goes up they have to pay more taxes, so they're incentivized to ban anything new from being built.

I totally understand the rationale. My problem is that I don't see it happen in real life. Where I live, quite a lot of new high-end housing has been built, but it hasn't seemed to reduce housing costs at all. The people moving into the new housing aren't vacating lower-cost housing to do so. They're mostly people moving into the area for the first time.

So housing costs for everybody, but mostly at the more affordable end, continue to rise faster than inflation.

We would have to calculate the rate of influx vs construction. There are places where there is a lot of construction but the new construction still isn't enough to keep up with demand so instead of reducing prices it just slows down the increase. In your example I would guess if that high-end housing hadn't been built the increases would have been steeper and the new arrivals would be displacing the people in lower cost housing

Yes, I understand the theory. But after decades of watching this stuff, the topic kind of falls into "what am I going to believe, the theory or my lying eyes?" territory.

If I saw this effect actually happen over the long term, I'd be less suspicious of it. As it is, I'm very suspicious about it. I'm not saying I think it's not true, I'm saying that I haven't seen any indication that it is.

The point is that housing costs would have gone up more if that housing wasn't built, not that some amount of built housing automatically means prices grow slower than inflation.

It just means that we need to build even more new housing to keep up with the demand, and that the situation would have been even worse if we hadn't built what we have.

The problem is that there is not enough housing for the people who want to live there. Building more is the only way to address that problem other than exclusing people who want to live there.

But the problem is that there is little economic incentive to build more than is being built. The housing is being built for wealthy people. If most of those people aren't trading up from less expensive units, then that doesn't vacate any less expensive units. So, outside of the wealthy crowd, there is little downward price pressure in housing.

If the new housing hadn't been built, that new class of buyer would've just displaced the residents of older housing, and you'd get the higher prices but for shittier housing stock. This is why a 1BR in a run-down low-rise in Silicon Valley goes for $2200/month and the Bay Area's working class lives in Sacramento or Stockton.

> They're mostly people moving into the area for the first time.

Then instead of moving into the new high housing, they would have offered similar to what they are paying for the high end housing for the the lower cost housing people are in now driving the price of that up. The people living in that tier, May have been forced to a yet lower tier, driving those prices up, and so on.

In my experience a rising tide lifts all boats. New "luxury" housing sets a new price for a neighborhood, which attracts flippers and investors who turn the old, cheaper stock into old, expensive stock. The rise in price of the old stock also increases the price of the new stock because of (hand wave) "comparables" and some people just want the biggest and newest house.

Maybe this wouldn't happen if we had all the stock we needed, but from what I've experienced it seems like adding new high priced housing to a supply constrained market increases prices rather than reduces them.

There's endless housing being built where I am, but it's all massive 4-6 bedroom, 4 car garage monstrosities that nobody but the 0.1% could afford to live in, and meanwhile service industry folks can't find enough places to live so they're having to drive an hour+ to get to the area to work.

Even if it were practically given away, nobody but the ultra-wealthy could afford the taxes on the huge chunk of land, the utilities, or the upkeep.

The argument for building "any" housing is just trickle-down bullshit based on the notion that lots of wealthy people are hanging around in housing that others could afford. Except that by building more housing for the wealthy, you lift that area up - there's more market and demand for luxury shops, services, and so on..so commercial real estate becomes more expensive, and so on.

The other reality is that people in luxury housing don't like non-luxury housing near them, so they do things like buy up property near them, tear it down or renovate it, turning it into more luxury housing.

Housing builders don't want prices to fall. Nor do the investors who fund new construction and buy existing houses. In other words, the general public are not the ones you need to convince.

EDIT: Nor do existing homeowners want to see their house prices fall. So anything that relies upon them voting to change the value of their homes is a non-starter too.

Plus, houses are touted as a major investment vehicle for the average citizen. If they all go underwater due to lowered prices, it'll result in a pretty big economic crisis. So most government agencies won't want to see house prices go down too much either.

No, but they want to profit from the existing prices, which they do by building new ones. Builders earn their money by building, not by gloating over the prices.

You're making a lot of bold claims in this thread based on this 10% figure. But what's the evidence that builders are doing this as part of some sort of strategy to keep prices high and not a normal level of vacancy due to turnover and general market inefficiency? (Some assets in all markets will be overpriced and not sell immediately. How do we know that 10% is too high?)

Your theory also ignores the fact that builders have other ways of investing their money. Why build a house and let it sit vacant when you could have just not built that house and invested the money elsewhere?

builders would always prefer to build more and sell more, if a home costs me 200k to build and it currently sells for 500k but current regulations only allow me to build 100 of them then that's $3m profit (actual margins aren't this high).

if a law comes along that suddenly gives me the power to build 200 but the asking price drops to 400k i'd rather build 200 homes and net $4m

All things being equal, companies want to sell as little as possible for as much as possible. We all want to make the most amount of money with the least amount of work.

You also need to factor in the time it takes to build a home. If I can build 100 homes a year I'd rather take $3m profit each year than build the cheaper homes for $2m profit. Sure, if I can scale up infinitely, then I'll go ahead and build infinite homes for infinite profit. But in the real world there is significant risk in scaling up. If I build too many homes and the prices go down, then I'm now hurting my own profits. It can be better for me to do the lower effort thing and build less for a higher profit margin.

Not to sound too much like a marxist, but @falcolas has a point here. If builders were offering a public service, they would likely sell their new homes (condos, townhomes, high-rises, etc.) for cost plus a reasonable percentage. But new homes go into a speculation market where the exchange value of the home factors in profit by the rentier class who add nothing to the value of the transaction.

> the rentier class who add nothing to the value of the transaction

I lived in one of the most expensive rental markets in the US for a while, so believe me, I'm not inclined to defend landlords, but the availability of rental units do serve a function. Even if we make the crazy assumption that a law forbidding the ownership of more than one residence would have resulted in a median home price one-third of what it actually was in my market, for half the time I lived there, I couldn't have afforded a down payment and a mortgage, and for the other half, I wouldn't have wanted to. There's a risk in tying up a significant chunk of your net worth in an illiquid asset.

For what it's worth, I believe rent-seeking (in the economic sense) behavior should be heavily discouraged as a matter of public policy, and believe that a system of taxation that is centered around land-value tax is the best way to achieve that, at least for residences.

> a public service [...] for cost plus a reasonable percentage

This type of regulation only makes sense for natural monopolies like utilities and whatnot.

The only parallel is that Marx also reasoned with a simplified, “armchair-economist” understanding that failed to account for credit, innovation, competition, risk, and return, among other things. Each of these are fundamentally critical aspects of the real economy, far better understood and articulated since his work. In modern times, we recognize Marxist principles are primarily designed to create disruptive but centralized authoritarian systems.

Marx's Das Kapital third volume is about the effect of credit and competition in a capitalist economy. Innovation and why it develops so much more in capitalist economies than in previous systems was something considered already in the first volume, like risk and return and how these are not the things that justify the capitalist profit. Marx also wrote very little about creating any system, only pointed general tendencies as part of his dialectics. Marx work is the culmination of classical economy, so much that is very hard to find a third option besides either abandon the core classical economy principles or becoming at least partially Marxist. While one could always disagree with the tenets of classical economy, and nowadays the great majority of economists are from other schools of thought, most attacks against Marx reverberated over the Internet are very unjust, originally formulated more based on political bias than on a real understanding; and then, they are inadvertently repeated by the dynamics of the Internet.

“Plus, houses are touted as a major investment vehicle for the average citizen. If they all go underwater due to lowered prices, it'll result in a pretty big economic crisis. So most government agencies won't want to see house prices go down too much either.”

That’s a big problem. A lot of peoples retirement plans rely on the value of their house. I am one of them.

Builders don't make money on the resale of existing homes. They want new homes to fetch the highest price, but they can also earn money on volume. Nothing built, nothing sold. Existing homeowners are the blocker.

And increased construction doesn't mean home owner go underwater. That's a pretty extreme situation. Housing prices are unlikely to drop barring a disaster like 2007. Houses will become affordable even if the prices rise more slowly. Encouraging home ownership as a means to increase wealth really has to go away. It's the major contributing factor to the aforementioned reluctance of existing home owners.

Seriously. So many people have a low-information understanding of the housing market, and think that homebuilders somehow aren't rational actors. Why would people who make their money building houses be into lowering their profit margins and causing pricing shocks for their existing stock of houses that are in construction? Developers are incentivized to charge what the market will bear. It is public policy's job to reform the incentives so other market players see opportunities to build lower-priced and lower-margin housing stock - I think the best way to do this is to make public lending corporations that will provide 3% construction loans, which are far more attractive than the 8% to 10% presently charged by institutional lenders. Couple that with expedited permitting for these projects, and tie them to affordability standards, and that's a market disruption that makes sense for most people. But simply deregulating and hoping that prices will fall never, ever works.

> Nor do existing homeowners want to see their house prices fall.

In my area, people who own homes to live in (rather than as investments) love to see their house value fall because it reduces the amount they pay in property tax.

If my house value falls, broadly speaking, other ones fall. If my house value raises, broadly speaking, other ones raise.

Buying a house means, generally speaking, I can kinda "guarantee" I can afford that "quality" of house. It's like having a housing share that I can exchange for another similar house.

Starting homeowners who might want to move into a bigger home do want prices to fall as well. The loss in return of your current home is being royally offset by reduction in price when buying.

A lot of US cities are already spread out a lot. But businesses don’t spread very much but concentrate in a few hot spots. That leads to very long commutes. If remote work doesn’t become much more common people can’t move into that empty space because there is no way to earn a living there.

Certain social circles wants to live near each other. Moving away simply isn't an option in their head space. It would mean abandoning what they consider their family.

A vacant 2 bed room 1 bath house in Mansfield Ohio does not help the family of 5 in San Francisco let alone Cleveland. Where the vacancy is and the “quality” so to speak matters a lot.

Additionally, some percentage of homes have to be vacant to allow someone to move into it. You will need to provide evidence that the vacancy rate of a specific market is causing prices to go higher. Citing national statistics when talking about a local issue does not help.

Look at my post immediately previous to yours. It links to a Lending Tree study that indicates an inverse relationship between vacancy rate and median home price. Hawaii is an obvious outlier, but interestingly, so is New Jersey. (What's going on in Jersey?) The data in this study is broken down by state; SMSA would probably be better, but I didn't spend a lot of time digging up data.

That data backs up what I am saying though. The national average means nothing, even state averages means nothing if where you are looking for housing, the vacancies are either not high enough to facilitate moving people around or are in conditions or floor plans that do not fit your needs. Not every vacant unit of housing is equally fungible.

California having one of the lowest vacancy rates and one of the highest median housing rates means there potentially needs to be a much higher rate of vacant units to lower housing prices if they are as inversely related as you describe.

If you trust the data (some of which comes from the 2020 census), it implies a nation-wide vacancy rate of 11.67%. Which was lower than I suspected, but higher than @falcolas' guess at 10%.

Also... I think I saw something go by indicating prices were still falling, at least in some markets.

Though that last one is a little confusing, citing data from the last three months in one section and data over 2 years in another. But it does (at least) make a nod towards explaining pricing in terms of supply and demand. I assert, and I think this is similar to @falcolas' point, that participation in the market by builders, foreign and domestic investors and banks has veered US house pricing noticeably away from true elasticity.

I do not damn builders for trying to increase their profits. We're a "wealth creation" economy, after all. But there does seem to be some conflict between stated national policy objectives of "affordable housing" and "profitable housing market." Alas, I bemoan the erosion of sensible policy-making in Washington. In the old days we would have just come out and said something like "we have affordable housing targets and will manipulate the market to achieve them." Now we're too spooked to say anything lest we upset the markets; or at least it seems.

Necessary for someone to move into that city, for one thing.

In practical terms, also necessary to facilitate the functioning of the market. Most homes are sold by living people (rather than by their estates). They can't sell their house without someplace else lined up to move into.

Ah. I thought we were talking about new homes, which are sold by builders (or the bank if the builder goes bust.) On the secondary market, opportunities for weirdness certainly exists. Investors buy older homes as well as new. And my sense is fewer people are looking to buy homes in this market with mortgage rates having gone up recently. I think people who don't HAVE to sell their homes are waiting it out until rates go down and they think they can get more for their home. I have no data to back that up, it's just anecdata from talking to a few realtors and noticing there are fewer homes listed on zillow in areas I've been looking at for the last several years.

Which is to say... I think there's less inventory than we would have seen had rates remained lower. But that's sort of unrelated to the issue of builders manipulating their rates of inventory creation (which I can't imagine they don't do, at least in response to macro-economic conditions.) The reason I think they should be treated differently is it takes a noticeable amount of time for a builder to build a house. First they have to negotiate financing and insurance, negotiate plans with the county, recruit a construction crew, etc. Home owners in the secondary market can respond to market conditions much faster.

I'm having trouble reconciling this with the fact that in my corner of the world prices have been growing exponentially during the past decade despite the population remaining relatively stable and a record number of housing units being built.

The only thing that changed in this period was investment demand, which skyrocketed.

I have a building in my neighbourhood which consists solely of tiny studio apartments - the vast majority of which were already bought out back when the project was still a hole in the ground. Half of the lights are perpetually dark, because barely anyone lives there.

Or better yet: there's a hole in the ground in my neighbourhood that was still the previous building back when they started selling apartments - the company went bankrupt during the pandemic and construction was only started when another company stepped in and bought everything.

Bottom line is you can't fight exponential growth in demand with linear increase of supply.

This. We're still in the midst of an asset bubble due to fiscal and monetary excess. Monetary policy changes haven't largely taken effect yet while we are still stimulating the economy on the fiscal side with deficit spending.

Vancouver has one of the least affordable housing markets in North America and people have been concerned about it for years. 4 years ago, it was even a municipal election issue, yet most people who couldn't afford housing voted in some of the most NIMBY councillors, who in turn voted down any significant housing project. The reason? New units are expensive, so building them makes housing more expensive. Even some smart, educated people couldn't see past this.

I attribute this to the pervasive publishing model where anyone can submit an article to any publication, and as long as the topic lines up with current events, then the editor is just a bot that is checking for spelling and the headline being clickable.

Induced demand is real. Building a desirable house may cause somebody to move to a city that they wouldn't otherwise move to.

But the article is more than its headline. It comes armed with data that shows that the induced demand effect is not significant in the markets studied.

Perhaps this is true on average over all housing classes, but in my university town, there has been a tremendous increase in supply (luxury appts for rich undergraduates) and no decrease in costs. And now there is a proposal to remove all R-1 (residential) zoning, so large appts can be build anywhere, all in the name of making housing more affordable.

But past increases in supply have not made housing affordable, and the effect will be to convert older smaller (cheaper) single family homes into apartment complexes that are designed for students, not single families. It seems pretty clear that the up-zoning will not make housing affordable for the middle class. Perhaps it will be more affordable for less price sensitive students.

The scope of potential impact from building luxury apartments is wider than a price decrease. It' likely your area has a far larger demand for housing than the amount that is being built + existing housing stock, regardless of type (luxury vs affordable).

Put another way, building the luxury apartments helped prevent an acceleration of price increases across all levels of housing stock. Students from high income families need a place to live, and instead of taking housing stock from the affordable pool, further driving up costs, they have additional desirable supply at their income level.

But! That only prevented price increases due to limited additional supply and was insufficient to drive down costs. Overall aggregate demand still exceeds supply. The simply answer is to build more at all price levels. Small incremental increases of supply are unlikely to drive down costs.

Besides the other commenter's point (that had the apartments, luxury or otherwise, not been built, prices would have gone up), I think college towns are an exceptional market, especially depending on what type of college it is. If it's an elite, highly selective university, a lot of the students going there are largely price-insensitive. Same for universities with a lot of foreign students.

And in general, college towns are highly desirable places, with a blend of small-town feeling and cultural amenities that punch way above their weight due to all the students. It's hard for prices to fall in situations like that.

You're assuming prices wouldn't have increased by even more if the apartments weren't built. I'm not sure why. Increasing supply has absolutely made housing more affordable relative to where it would be if supply hadn't expanded. You're just not expanding supply fast enough to see a decrease in cost.

Perhaps more affordable on average, but if the apartments replace older smaller single family homes, then the supply demand thesis suggests that those single family homes would become less affordable.

So yes, things become cheaper if everyone wants to live in an apartment. But for modest income folks in small old houses, up zoning means moving out of the community.

By the pigeonhole principle not everyone who wants to live in a growing city can own a house. So long as houses are allocated economically (as opposed to submitting an application to join the queue at the People's Bureau of Housing or whatever) this will reveal itself as some people being unable to afford houses. So we can conclude that the affordability of single family homes in isolation isn't the problem we should focus on.

> So yes, things become cheaper if everyone wants to live in an apartment.

People make tradeoffs all the time. Lots of people would love to own a nice house in a nice neighborhood within walking distance to a forest and to downtown for not very much money. But too many people want to live there for them to all own houses. So some will choose to live in an apartment instead, and others will choose to move farther away to be able to own a house. Preventing upzoning will just mean that fewer people get to make the tradeoff to live in that neighborhood, and only the richest of them will be able to pay through the nose to do so.

> But for modest income folks in small old houses, up zoning means moving out of the community.

Well, nobody's forcing them to. After their house has been upzoned they can live in it for as long as they want, then sell it to a developer for millions of dollars when they want to move. The developer will use the land to build apartments, and sell them to people who don't have a million dollars to buy a house. Everybody wins.

Interesting to hear that zoning ordinances are equivalent to the people’s bureau of housing.

And nice to know that the market serves everyone (if they have enough money), but those retirees in their little house will be moving out, because they will not be able to afford the property taxes. So actually, the “market” is forcing them out.

It is also interesting to hear the argument that even though increased supply has not slowed (and may have accelerated) housing prices, we should ignore that data, because theory tells us that in the absence of increased supply, prices would have risen even more. That’s a difficult point to argue, since it seems more like faith than fact.

I know it's off-topic, but I can't help noticing Financial Times pricing model. It's $1 for 4 weeks, $69 a month for digital, but also $99 a year for print and digital? That's a wild pricing model.

I long for the day that I can just pay XX cents to read a single article with minimal fuss, but at this point I don't see that happening.

Looks almost like a typical "good better best" upsell to me, trying to get you to go for the "better" option. But they turned it into a variation to get you to accidentally subscribe to the "better" option by also having a cheap trial ($1 for 4 weeks).

In Toronto, the number of condos that have been built is staggering. There must be hundreds of thousands of new condos in the last 20 years.

The prices have only gone up. The idea that new housing reduces cost is insane. All of the condos being built are at the top of the price range.

What needs to be done is NEW CITIES need to be created with business centers. Not adding more housing into already packed cities.

I have been saying for a decade that large tech employers like Google and Facebook should have created offices in the middle of the US, which cheaper neighborhoods, better schools, etc. Create opportunities for families to move out from the tech areas and enrich other parts of the country. But they keep doubling, tripling and quadrupling down on the Bay Area.

New cities need to be created with business centers, not new condos in old cities!

I mean, imagine what housing in Toronto would cost if they didn't build those 100K+ condos? Pricing is composed of supply and demand, and the article is saying that holding demand constant, increasing supply lowers prices. Adding a marginal unit to the housing stock kinda has to result in lower or equal prices in the static case.

Toronto is growing insanely quickly, and supply can't meet demand. New cities are great, but a large number of people want to move to big and established population centres.

We are in violent agreement. Creating new condos will still keep the prices increasing, but it will be better than the situation where no new housing is built.

But the article specifically says "new homes reduce house prices." This is patently false.

Toronto is growing because there's no real business centers outside of Toronto for the 1 million immigrants a year that are coming in. We need to create viable options by expanding business outside of Toronto in new land, so that housing demand lessens.

FAANGs are not doubling down on the Bay Area. Several of them are making significant expansions in Austin, North Carolina, Virginia, Colorado, etc. I was told specifically by an Apple recruiter a couple years ago that they were told to concentrate recruiting outside of Cupertino.

more housing does decrease prices. the price went up, but not as much as it would have. for us to see a.price decrease, we would have to see new buildings out pace new people to the area for a sustained period of time. and what is more likely to happen is that they won't decrease but stay flat.

staying flat is still a price decrease each year it does it.

I think we're dealing with multiple overlapping issues in the housing sector. For example, where are we going to get enough skilled trades to build the houses? There are many reasons why trades are in short supply from lack of interest to immigration enforcement.

I think lack of pay is a big issue as well. (most) everyone has a number where they'd get on a ladder and learn say roofing, but it's typically much higher than $22.50 an hour.

Wages are certainly part of the issue. The job certainly wouldn't interest me at that rate, forever. Skilled trades do better, however there's a lot standing in their way. Getting started, there are easier jobs with better _starting_ pay.

Even before covid and the following inflation, there was a serious problem with brain drain in the industry. This Old House set aside time for every show to recruit younger participants.

Not true if new housing stock is snapped up by speculators/investors/foreigners. Housing, like freeways, can suffer from induced demand, if the target market of the housing project is for people who do not live in the project's geographical region.

It can't be this simple. I know that at a strictly mathematical level it feels like it must be true, like the "Calories In = Calories Out" model of weight loss, and yet, like CICO, feels useless as a principle.

(CICO's problem: as a mathematical relationship it has to be true, but it's too dumb to be helpful: what controls calories out? all of: exercise + resting metabolism + how many calories you hold onto + how much you exhale + how much you excrete, and most of these are regulated by your desire for exercise, eating, etc. -- so while it is the value of d(weight)/dt, it tells you nothing about the first-order term that you should actually control; it's a mix of terms of different orders.)

Similarly, there are clearly multiple "first-order effects" at play that are producing the final housing costs. It's not the case that there is one first-order effect, supply and demand, and then a bunch of 2nd-order corrections. I wish I could clearly see what the full equation is though.

My poorly-informed guess is that the actual first-order model looks like this: "real inflation" is actually much higher than the reported numbers and is best reflected in housing prices (and healthcare prices). The reported number of inflation is much lower because certain sectors --- electronics, food, and other mass-produced consumer goods --- have had their prices heavily suppressed by exploiting global economies or controlled by policy. So lower-income workers, because they can afford smartphones and food, don't feel as poor as they actually are. But housing prices are tracking money supply, which is mostly (incredibly disproportionately) going to high-earners, like many of the tech employees here and all the economic winners of the last fifty years; the incongruity explains why everything is so expensive. At the margin, more supply just gives the rich people more places to park their money -- because they have so much money. I expect that's the best model of e.g. Toronto and NYC.

Put differently: if you took tech salaries and San Francisco rents and divided them both by four, they'd feel like reasonable numbers. Everyone else is getting burned by that.

No. It really is that simple. There are x units and y people looking for units in an area. If we had enough housing it wouldn't be seen as investment because the returns would be terrible since landlords would be competing for renters instead of the other way around. Leaving housing vacant only makes sense if you've cornered the market or are a land speculator. Most American cities do not have a cornered rental market so we just need to stop land speculation.

I think you missed my point entirely. I'm saying that supply-and-demand is too simple to be useful, not that it is untrue. It does not point directly at the dominant effect that is causing housing to be priced the way it is, although it is part of the overall equation. I still believe that building lots of housing is a great idea (and finding a way to make more cheaper non-luxury-priced housing get built would be even better). But it's not a good-enough theory of housing prices.

The basis for this articles' argument^ is not really empirical. It's theoretical. And rational in the sense that it models theory to create predictions... It is quite a cherry-picked collection of published studies, not a metastudy.

Anyway, the crux of theoretical argument is "supply and demand... duh." This is often true, depending on the market, but... it really depends on the market. For real estate, "focusing on supply" often leads to understating the significant "out of theory" factors.

For example, real estate "demand," is largely determined by mortgage availability. That's the source of funds. Besides this, British real estate is an investment class with prices affected by rates, performance of other asset classes, and such. These are big factors.

Dublin city, not far, basically conducted an unscripted experiment in this space during 2008-2015. Lending collapsed. Demand collapsed. Lending was gradually restored, and median house values tracked median approved mortgage max outs. IE, if the average bank agreed to lend $X to the average applicant with an average income... that became the average price. Where the banks (CB, really) created subcategories with special rules (eg single bedroom apartments were mortgage disqualified for a while), those special rules dictated average prices for those categories.^^

This is not surprising when you consider the various leverages and flexibilities of the demand side, compared to the flaccid supply side of the equation.

"When asked about the impact of a 10 per cent increase in regional housing supply, however, 40 per cent say prices and rents would rise, while only a third say they would fall."

Sounds to me that most people just guess. But... this is a disingenuous frame. A 10% increase in (London) housing supply doesn't happen often. That's the point. When it does happen, it rarely happens unless prices hold up. There is no realistic scenario where London is exploding into the sky while a flood of supply crashes prices. This is tunnel-vision, model-only thinking. The supply "lever" he wants to crank is good for fractions of a percent, not 10%.

None of this is to say not to build. If we don't build housing, we cant have more housing. But, house prices are not made in the the council's planning permission basement. This is fantasy.

^"Studies show" is a cop out. Make the argument yourself. Base your arguments on the studies, if convincing. Shots fired :-)

^^In Ireland, this has led to the opposite extreme, and equally erroneous belief that supply is always irrelevant to price.

If you build a $5 million dollar house, and a multimillionaire buys it as their fourth house, this does not reduce housing costs for anyone.

If you build a thousand new apartments in Sri Lanka, this has no practical effect on the cost of housing in Colombia.

If a housing authority pays a contractor to build a dozen affordable, subsidized apartments, but the apartments are then discovered to be uninhabitable firetraps, the cost of housing can go up.

Authoritatively making sweeping generalizations not only ignores the edge cases, it often sets policy in ways that enable more of those edge cases.

> If you build a $5 million dollar house, and a multimillionaire buys it as their fourth house, this does not reduce housing costs for anyone.

That’s not necessarily true. If you build a $5m house where there was previously no house, and the multimillionaire buys it, then they’re not buying some other $4m house, and someone could buy that instead of something else, etc.

For this to work, you need a situation where building n houses does not create demand for approximately n houses.

Well no, the demand is so high that your proposal makes no sense:

1. High demand on labor and materials from builders makes the cost of labor and materials go up

2. If the demand for the actual home reduces, and the cost of labor does not go down because those workers are now offered better prices as a Walmart worker, material costs may go down, but since materials are about 25% of the cost, it will make the price of the house go down very little.

3. The airbnb/landlord/second-and-third homes from Google stock holders demand seems to be insatiable. If that changes, the entire thing may then finally collapse. However that collapse is much more likely than builders being able to supply the housing with labor and material costs so high right now.

Article is subscription locked, so I just read the (patronizing and reductive) headline.

The problem never has been lack of housing. The problem has always been lack of land. You can only build new homes on existing land and nobody wants to repurpose existing land to build new houses. Where exactly in NYC can we build new houses?

And what houses are we talking about? Single family houses that are not a good use of land? Huge multifamily complexes that further stress the crumbling infrastructure?

Housing costs are not my top priority for my QOL. Building more houses will likely impact me only in negative ways.

And again, the article is subscription locked so all I can do is read the headline.

Those places would rise in price slightly slower with more supply. It's not like the housing stock is inducing enough demand to affect the price; the demand comes from other desirable characteristics like access to good jobs and weather.

In SF at least, we are severely supply constrained. Increasing the supply hasn't been tried in meaningful numbers to know for certain how it could affect price. But in many other municipalities that have been better able to build housing, it does decrease costs for everyone as the article describes.

It doesn't unless it is outpaced by the increase in demand for housing. This person makes it sound like they have a ton of brand new houses in Austin with nobody living in them because they're too expensive. I can tell you as a former Austinite, that couldn't be further from the truth.

Induced demand, the same mechanism by which building more and wider roads doesn’t always mean less traffic. There’s still only so much land and space in a given area, and even in high density areas there are more and less desirable spots (e.g. a penthouse suite vs a basement apartment next to the furnace). As more people move into an area, more competition for those desirable spots has an increased pressure on the prices for those spots, which in turn increases prices for other less lucrative spots because the whole market window is shifted.

that sounds vaguely plausible, but is there any evidence for it other than sounding vaguely plausible?

it seems like the other explanation there is simply that most cities aren't building more housing fast enough to meet demand. there's been a longstanding population shift to urban centres that's consistent enough across all major cities that i don't think it can be easily explained as induced demand from homebuilding. especially since most cities aren't building all that much new residential.

Well let’s talk about what it would mean for prices to go down. We’re in agreement that not building enough to meet demand will drive prices up. So why is that so? Well we can think about what demand is, it’s people already living in the area that want to move (perhaps because they’re renters looking to buy), it’s people outside the area looking to move into the area and it’s investors/rental landlords looking to buy because they anticipate an increased demand that they will be able to profit from by selling or renting to future demanders from one of the first two categories.

So in order for prices to go down, you need to have a 0 or negative expected future demand to eliminate the incentive for the investors. But if you have negative or 0 expected future demand, then you also have no reason to build new houses at all. No one is going to spend tens or hundreds of thousands of dollars to just sit and watch the building rot away. Either they expect to sell it or rent it after it’s built, and you can only do that by either having demand outpacing supply or anticipating demand in the future that is higher than the current demand. If we had a magical perfect equilibrium between demand and new supply, at best prices would remain steady/only increase with inflation. The only mechanism by which new building can reduce the costs of housing is to build more housing than both current and all anticipated future demand.

It's not inconceivable. There's obviously some agglomeration advantage. People are valuable to other people. For instance, I think if SF built sufficient new homes it would have a lot more young people and they'll make the place nicer and that will make it more valuable.

{kind=link}

{kind=link}

The only way to incentive construction is to incentive construction. NYC HPD is an agency, for example, that has a history of providing low interest rate loans for approved projects to rehab old buildings. With borrowing costs hovering at 8%-10% for new construction projects, and with lenders tightening standards, this is the perfect time for state governments and the federal government to provide 3% construction loans, accessed in tranches after milestones are met, to facilitate not only housing on the cheaper end of the spectrum, but lower-margin housing projects that established developers and big lenders typically shy away from.

Simply deregulating does not work, and it's foolish to think it would. Lower cost housing, made profitable by public lenders as a last resort, is a no-brainer that gets lost in the discussion. As is rent control, by the way. But that won't lead to the same cast of characters getting boffo bucks through deregulation, so neither option is taken seriously by Serious People.